Home equity line of credit (HELOC) rates have edged higher today. Homeowners with low primary mortgage rates may want to hold off before tapping into equity

Home equity line of credit (HELOC) rates have edged higher today. Homeowners with low primary mortgage rates may want to hold off before tapping into equity

📊 The Latest: Rates on the Move

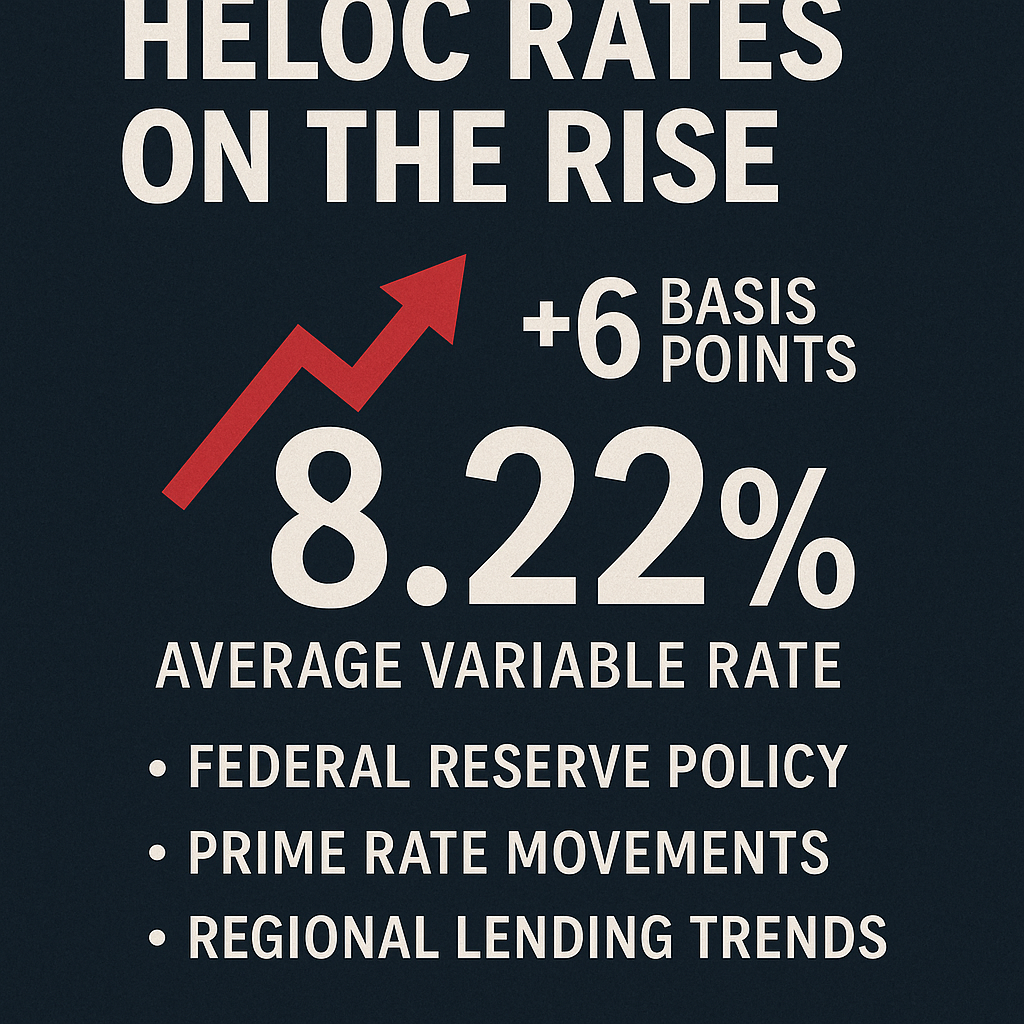

Home Equity Line of Credit (HELOC) rates nudged upward slightly today, marking a notable—though not alarming—development in the lending landscape. According to market analysts, the average HELOC rate has climbed by approximately 6 basis points, now sitting close to 8.22% nationally for variable-rate offers. This adjustment may seem minor, but it can significantly impact borrowing costs over time, especially for large credit draws or prolonged repayment plans.

This modest rate increase reflects ongoing financial market volatility and the broader economic uncertainty surrounding Federal Reserve policy, inflation trends, and banking sector lending behaviors.

💼 What is a HELOC, and Why Should You Care?

A Home Equity Line of Credit (HELOC) is a revolving credit line secured by the equity in your home. Think of it like a credit card with your house as collateral—but with lower interest and larger borrowing capacity. Unlike traditional home loans, HELOCs often come with variable interest rates, which means the monthly payment can shift with the market.

HELOCs are popular for:

Renovation projects

Emergency funds

Debt consolidation

Tuition or educational costs

But as rates rise, borrowing becomes more expensive. The recent uptick may push some homeowners to rethink their renovation timelines or debt repayment plans.

🧭 Why Are HELOC Rates Increasing?

Several factors contribute to the recent shift:

Federal Reserve Policy

Although the Fed hasn’t raised rates recently, it has not signaled immediate cuts either. With inflation hovering above target and global uncertainties continuing, lenders are cautiously pricing future risk into HELOC products.

Prime Rate Influence

HELOCs are typically tied to the prime rate, which itself is influenced by the Fed’s benchmark interest rate. Since the prime rate hasn’t moved significantly, most of today’s adjustment reflects lender-specific strategies or cost-of-capital recalculations.

Regional Lending Trends

In some areas, particularly those with fast-appreciating property values, banks are tightening conditions or tweaking margins. This includes slight rate bumps to balance supply and demand in credit markets.

📌 Fixed-Rate Loans Still Offer Stability

While HELOCs are popular for their flexibility, home equity loans (which have fixed rates) remain a stable alternative. These loans currently average around 8.25%, offering consistent monthly payments and protection from market fluctuations.

For those who value predictability—especially in long-term financial planning—a home equity loan might be a better fit, despite slightly higher upfront rates.

📈 Small Bump, Big Impact?

Let’s break it down:

For a homeowner borrowing $50,000 through a HELOC at 8.16%, the monthly interest-only payment would be around $340.

A 6 basis point increase raises that to approximately $344—a small jump, yes, but over 10 years, this could amount to over $500 extra in interest.

Now imagine that same rate change applying to a $200,000 credit line. The impact compounds.

🛠️ Renovating? Here's What to Consider

If you’re planning a kitchen upgrade, bathroom remodel, or full home extension using your HELOC, timing is critical. Many contractors report material prices stabilizing after years of volatility, but labor costs remain high.

Combine this with rising credit rates, and the “wait-and-see” approach may cost more than acting now. On the other hand, if you can wait until later in the year, you might benefit from potential rate cuts, if inflation eases and Fed policy softens.

💬 What the Experts Say

“Today’s increase isn’t shocking, but it’s a reminder that low-rate windows don’t last forever. Borrowers need to shop aggressively, compare intro rates, and consider repayment flexibility.”

— Amanda Reyes, Senior Analyst, Mortgage Watch

“In 2025, we’re entering a ‘cautious optimism’ phase. Borrowers have more options, but lenders are moving more conservatively. Your equity remains powerful—just use it wisely.”

— Brian Martin, Equity Loan Strategist

📝 Pro Tips for Borrowers

Shop Around

Don’t accept the first rate you’re offered. Different banks and credit unions have widely varying HELOC products, teaser rates, and closing costs.

Understand Your Draw Period

Most HELOCs have a 10-year draw period followed by a 20-year repayment period. Make sure you know how interest and principal are handled during both phases.

Monitor Fed Announcements

Even if today’s rate rise seems small, future Fed meetings could bring surprises. Stay informed.

Use It Strategically

Focus HELOC funds on value-adding renovations—like kitchen remodels, energy-efficient upgrades, or structural improvements—not consumables or depreciating assets.

🧾 Final Word

Today’s HELOC rate increase is a nudge, not a red alert. But it signals a broader trend: the days of ultra-cheap home equity borrowing may be behind us—for now. That doesn’t mean HELOCs aren’t useful—they remain one of the cheapest ways to borrow. But caution, comparison, and strategic planning are now more important than ever.

For homeowners, your equity is a powerful tool. The question isn’t just whether to use it—but how smartly you do.

Like

Dislike

Love

Angry

Sad

Funny

Wow

The Impact of Controversy on Top TikTok Stars: A Detailed Analysis

April 09, 2025

Ethereum's Ascent to New Heights: Analyzing Reasons Behind Its Record Value

April 08, 2025

Neuralink's Mind-Controlled Robotics: A Breakthrough in Technology

April 08, 2025

How a 10-Minute Full Body Workout Can Transform Your Fitness Routine

April 08, 2025

Sway Takes the Social Media World by Storm: Analysis of Its Rapid Growth

April 10, 2025

Comments 0